This expands on today's earlier post.

How much extra output do we get if we invest more?

How much extra output do we get if we invest more? Here’s

some rules of thumb.

1.

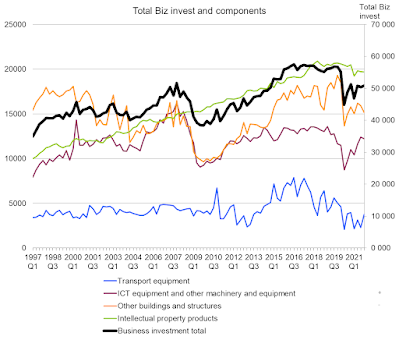

From the RF growth

mindset report, some useful data as background.

2.

Here’s our underperformance relative to the G7

3.

And here it is in bars:

4.

So we might regard our target is

a.

To get the US GDP per capita growth rates, we

need another 1.55-1.03 = approx 0.5% growth per year.

b.

Notice that’s relative to the USA, relative to

EU would be much less than that.

5.

How can we get to this via capital investment? Here’s the tyranny of numbers.

6.

The extra output from 1 extra unit of capital sounds

like an engineering problem. But we can

use some economic reasoning to get some measures.

7.

The average rate of return on capital is about

0.10 as measured by the ONS. That says

that the flow of profits from the existing capital stock in the UK, as a percentage

of that capital stock, is just below 10%.

8.

Let’s take a concrete example to check this. In Feb2024, according to IBA

Aero, the price of a new A320neo was $52m.

The monthly rental cost was $400,000.

This ratio is 9%. So that says

that airlines are incurring a cost of renting a new aircraft that is 9% of the

capital stock they would have to buy.

9.

If we further assuming that airlines are maximising

profits, then they would rent more and more aircraft until the extra flow of output

they can sell from renting another aircraft were equal to the extra costs. But we have just worked out the extra costs are

8%.

10.

That gives us part of the answer: for every

increase in capital stock by one unit, output rises by 0.08 units (0.1 units for

the economy as a whole)

11.

It’s more helpful to convert that into a

percentage. We can do this if we express

the change in output following a change in capital, the 0.1, as a proportion of

the baseline output/capital ratio. That ratio,

for most developed economies, is around 3.

12.

Thus we have the following:

a.

Average rates of return are around 0.1. This tells us the extra output from one more

unit of capital.

b.

Average output/capital is 3.

c.

So the percentage extra output from a one

percentage extra capital is 0.1/3 = approx. 0.3.

13.

What percentage rise in output do we get from a percentage

rise in capital then? For the economy as

a whole the rule is

% rise in output from x% rise in capital asset A= 0.3 *

share of capital asset A in the economy * % change in capital asset A.

14.

Let’s apply this rule to housing. It is planned to raise housing input by

0.3%. Housing is 40% of the total

capital stock. Thus the expected % rise

is 0.3*0.4*0.3% =0.036%.