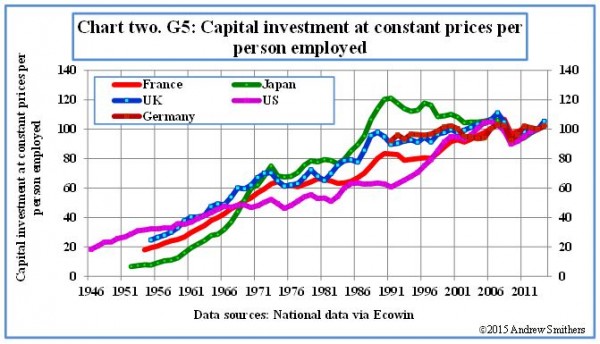

He then compares that with investmetn per person employed and observes that is rising, suggesting that investment must be less "efficient".

Productivity economists say that output per person depends on capital services per person and the efficiency with which that capital is used (there's also human capital, but lets just focus on non-human capital for the moment). So Ryanair produce a service of getting from A to B. They use planes, computers and check-in desks to do this, all of which provide capital services. They also try to use these very efficiently, with ticketless boarding, fast turnarounds etc.

The capital services in an economy is related to, but not the same as, investment. When Ryanair invest, some of their investment replaces worn out stuff. And if we want to calculate capital services, we cannot just add up investment in planes, computer and desks, since that's adding apples and oranges. We have to weight the capital by its flow of services that it provides: 10 computers and 10 desks don't yield the same capital services.

We also know that as economies develop they buy more and more machines so workers can work with more/better capital services (compare your computer now with that 15 years ago).

So what would you expect to see? First, capital services per employee would rise. Second,

you would expect a close relation between growth in value added per person employed and growth in capital services per person employed, with an additional kick from growth in efficiency.

To look at this, see below, I used the published Bank of England historial database which has the volume of value added (V, real GDP worksheet, column R) and employment and capital services (N and K, worksheet supply side data column B and E). The growth rates are indeed close, with the exception of the last year (2009). So that is just what we would expect it seems to me, and I'm not sure I see and decline in "capital efficiency", unless capital efficiency is defined in a way I don't understand.